Creditors’ Voluntary Liquidation (CVL): A Practical Guide for UK Directors

Read More

When your company enters liquidation, its physical assets, such as vehicles and equipment, are dealt with under specific legal procedures. A liquidator, appointed to manage the process, takes control of all company-owned assets. These assets are then inventoried, valued, and sold to repay creditors. This ensures that company property is realised and distributed fairly.

Understanding how these assets are managed helps you navigate liquidation confidently, ensuring compliance with UK insolvency law and minimising personal liability risks.

Get a Quick and Easy Liquidation Quote

Complete the form today to know how much it may cost and understand your next steps

✓ 100% Confidential | ✓ No Obligation | ✓ Licensed and Regulated Advice

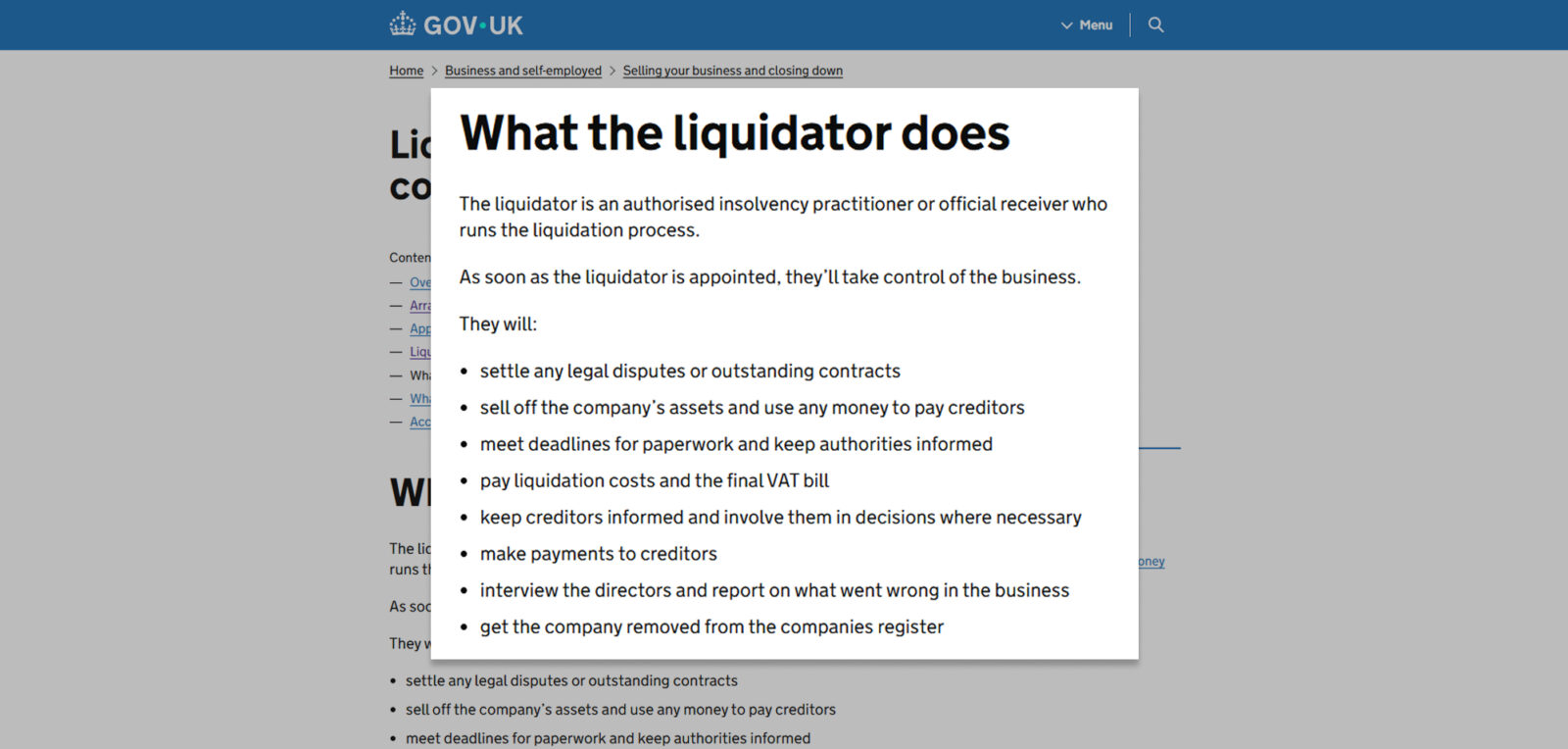

Assets are collected during liquidation to satisfy the company’s debts and legal obligations. Under the Insolvency Act 1986, the liquidator or Official Receiver takes control of the company’s assets to maximise returns for creditors.

The process involves securing company property, including vehicles, machinery, and other physical assets. The liquidator prepares an inventory, arranges professional valuations, and sells assets through auctions or private sales. In limited cases, assets may be disclaimed if they are onerous or unsaleable, such as contaminated land or items carrying ongoing liabilities.

By following this structured approach, the liquidation process ensures creditors are treated fairly and assets are dealt with lawfully.

The treatment of company vehicles in liquidation depends on their ownership or finance status.

Vehicles owned outright by the company form part of the liquidation estate. The liquidator will secure, value, and sell them, with proceeds distributed to creditors.

Vehicles under HP or finance agreements do not belong to the company until the agreement is fully paid. The liquidator must review the finance contract to determine ownership and equity:

Understanding this distinction helps you avoid unexpected liabilities and ensures compliance with UK insolvency requirements.

Handling equipment, machinery, and tools in liquidation follows a structured and legally defined process:

Full cooperation ensures a smoother process and reduces the risk of legal complications.

Get a Quick and Easy Liquidation Quote

Complete the form today to know how much it may cost and understand your next steps

✓ 100% Confidential | ✓ No Obligation | ✓ Licensed and Regulated Advice

Not all items in the company’s possession necessarily belong to it. This is especially relevant for assets subject to retention of title (ROT) clauses or owned by third parties.

Suppliers may include clauses stating that ownership remains with them until goods are fully paid for. If valid, these goods do not form part of the liquidation estate. The liquidator must review contracts and verify claims before releasing or returning goods. Selling ROT goods by mistake can lead to liability for the estate.

Leased equipment, consignment stock, or other items owned by third parties must be identified and returned once ownership is confirmed. Proper documentation is essential to avoid disputes.

By verifying ownership and communicating promptly with suppliers and third parties, the liquidator ensures compliance and avoids misallocation of property.

Valuing and selling company assets in liquidation involves independent assessment and transparent realisation:

This process ensures fairness and maximises returns for creditors.

The disposal of assets during liquidation triggers VAT considerations.

The sale of most company assets during liquidation is treated as a taxable supply. The liquidator must account for VAT where applicable, and the company remains VAT-registered until all taxable supplies are completed.

If assets are sold as part of a Transfer of a Going Concern, the transaction may be treated as outside the scope of VAT, provided HMRC’s TOGC conditions are met. These include:

Correct VAT treatment is essential to avoid penalties, so professional advice is recommended.

Get a Quick and Easy Liquidation Quote

Complete the form today to know how much it may cost and understand your next steps

✓ 100% Confidential | ✓ No Obligation | ✓ Licensed and Regulated Advice

Hazardous or onerous assets. such as contaminated land, waste materials, or items with high maintenance liabilities, can be disclaimed by the liquidator.

The liquidator may issue a statutory notice (Form NODIS) to formally disclaim the asset, relieving the company of further responsibility. Where hazardous materials or environmental risks are involved, the liquidator must notify relevant authorities such as the Environment Agency and the local authority.

This prevents the estate from incurring ongoing liabilities and ensures environmental compliance.

As a director, you retain important responsibilities during liquidation:

Fulfilling these duties protects you from potential legal consequences and supports an efficient liquidation process.

You can help ensure a smoother liquidation by following best practices:

These steps help maintain transparency and compliance throughout the process.

Get a Quick and Easy Liquidation Quote

Complete the form today to know how much it may cost and understand your next steps

✓ 100% Confidential | ✓ No Obligation | ✓ Licensed and Regulated Advice

1) Can I use company vehicles after liquidation begins?

No. Once liquidation starts, control of company assets passes to the liquidator. Using a vehicle without permission may lead to legal consequences.

2) Who handles vehicles under finance agreements?

The liquidator reviews the finance contract and decides whether to return the vehicle or settle the finance if there is equity for creditors.

3) What if finance exceeds asset value?

If the outstanding finance is greater than the asset’s value, the vehicle is usually returned to the finance company.

4) How do employees prove ownership of personal tools?

Receipts, personal purchase records, or employment terms specifying employee-owned tools can serve as evidence.

5) Can I buy back equipment from the liquidator?

Yes, at fair market value, to ensure creditors are treated fairly.

6) How long does it take to sell the assets?

Timeframes vary depending on asset type and market demand. The liquidator aims to sell assets efficiently while achieving fair value.

7) What if assets are sold below market value?

Sales are typically supported by independent valuations. Any concerns must be justified in the liquidation report.

8) Is it illegal to keep company equipment for personal use?

Yes, unless explicitly authorised by the liquidator.

9) What happens to intangible assets such as software licences?

The liquidator assesses their value and transferability. Some licences can be sold; others may be terminated or disclaimed.

10) Will the liquidator leave behind hazardous or worthless items?

Yes, if they are disclaimed as onerous property. Authorities are notified where required.

11) Can directors challenge a valuation?

You may raise concerns, but valuations are normally provided by independent professionals.

12) What documents should directors provide?

Receipts, finance agreements, contracts, and any documents establishing ownership or liability relating to company assets.